There are a myriad of ways in which the value of intangible assets can be calculated and these often depend on the goal of any such evaluation. Goals can be anything from a non-practicing entity calculating how much of a settlement they can gain from a patent after considering the costs of renewal payments and filing, to a bank deciding to loan a company funding on the basis of future revenue from intellectual property, or a mortgage on IP rights themselves, or when evaluating a company’s market value.

Amendments to Taiwan’s Statute on Industrial Innovation aim to provide a legal framework for the appraisal of intangible assets, including intellectual property.

The Statute on Industrial Innovation was first passed in 2010 and has been in effect for just over six years. Eighteen amendments passed into law in November of 2017, aimed at promoting industry innovation, attracting new investment, improving the industrial ecosystem and strengthening R&D capability in Taiwan, with an eye to international tech trends and bottlenecks in industrial R&D, land availability and a shortage of talent.

Among these are two amendments which aim to provide solutions for the appraisal of intangible assets.

The amendments address three core elements which affect the credibility of intangible assets appraisal, namely talent, organization and regulation. The amendments have made reference to the methodologies of the US, Japan and South Korea, implementing appraisal standards and management mechanisms to make appraisals credible, while also pushing for financial measures in the financial system that lower the fiduciary risk, and raise the willingness of financial institutions to provide funding and to encourage industrial development and the flow and exploitation of intellectual property.

However, the Ministry of Economic Affairs, which has now taken charge of supervising this sector has its work cut out for it if they are to realize the spirit of the amendment in establishing an industrial chain for the appraisal of intangible assets in a relatively short period of time.

On Dec. 20, 2017 the Business and Intangible Assets Appraisal Committee of the Republic of China Association of Public Chartered Accountants held a conference on the appraisal of businesses and intangible assets, introducing the mechanisms to be set up under the new amendments. Chen Kuo-hsien, head of the Knowledge Services Division of the Industrial Development Bureau under the Ministry of Economic Affairs, gave an overview of the challenges still to be faced in establishing an appraisal mechanism fit for purpose in today’s global business environment.

What Can Taiwan Learn from Other Countries?

1 Photo: Chen Kuo-hsien at the conference; Photo by Anita Li

1 Photo: Chen Kuo-hsien at the conference; Photo by Anita LiIntangible assets make up over 80% of the components of S&P 500 market value, according to an Ocean Tomo, LLC report cited by Chen, who added that the appraisal of intangible assets is becoming increasingly important in five major areas: domestic market transactions, financial reports, tax planning, internal management and in litigation. Chen stated that despite Taiwan's industrial transformation over recent years, the focus has continued to be on factories, equipment and other tangible assets. He pointed out that in emerging industries, such as IoT and AI, the proportion of intangible assets will get higher and higher. Chen added that unfortunately the domestic evaluation or appraisal system for intangible assets is not prepared for this, which means that intangible assets aren't being calculated in a reasonable way. This suggests that companies are unable to give a true representation of their market value. If Taiwan wants to establish a comprehensive system for the evaluation of intangible assets, the top priority is to find an objective and credible third party organization which can represent the value of these intangible assets.

Chen stated that the Industrial Development Bureau (IDB) has long been calling for businesses to register their intangible assets, but without a strong incentive for doing so, they have little motivation. "It's normally only when businesses face litigation that they will request the IDB to recommend an appraisal unit, or when they're applying for R&D expenses to be credited against corporate income tax payable and when companies show their intangible asset appraisal reports for tax credits they don't know who to go to for appraisals, which leads to several problems."

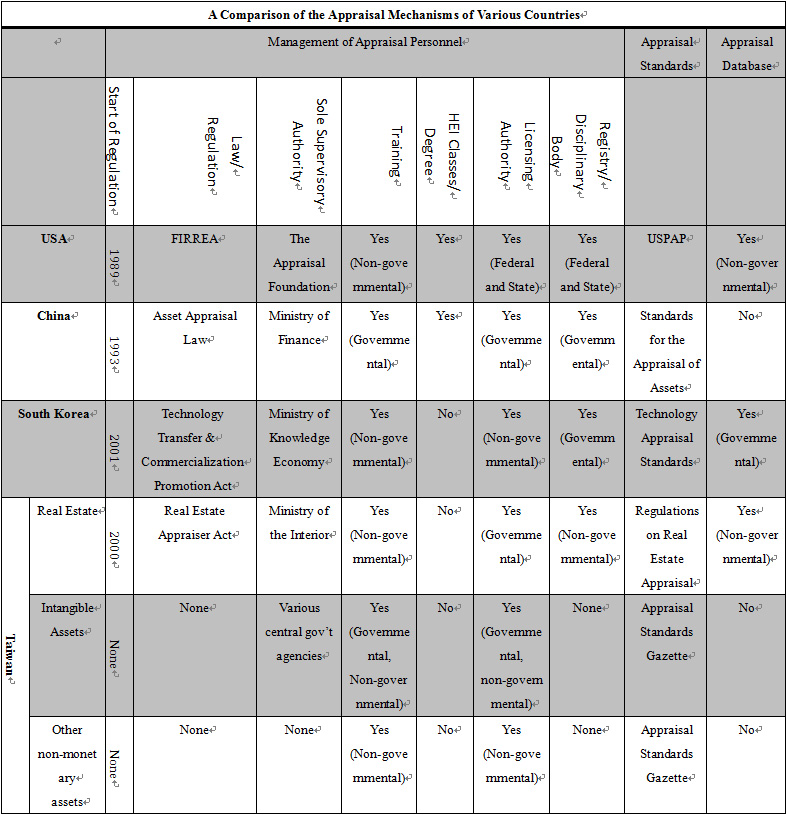

The chart below shows that the US has taken the lead in terms of appraisals on the world stage (See Chart 1) launching operations on this front back in 1989. As to Taiwan and South Korea, they have been involved in this sector from around about the same time, however Taiwan has not developed as rapidly. Chen pointed out in the chart denoting the asset appraisal operations of four countries that the appraisal of intangible assets has three characteristics: (1) There is a single supervisory body overseeing it; (2) There are dedicated laws or acts devoted to it; (3) The government registers and supervises appraisers and appraisal units.

Source: Chinese Association of Business and Intangible Assets Valuation; Translated by Conor Stuart

Chen stated that other countries have a comprehensive legal and supervisory framework in place for the appraisal of intangible assets. "If we cast our gaze back to Taiwan, however, it's clear that Taiwan has lacked a unified supervisory authority, as well as lacking standards for the appraisal of intangible assets, a database that can serve for reference purposes and credible appraisal entities and personnel, as well as a mechanism for managing them; in addition, it's also difficult to secure capital from intangible assets." he said. He added, "When the government was amending the statute, they communicated with all sectors and voices from all sectors were eager for the amendments to pass. This is most important in legal proceedings, as often judges will ask what the standards of appraisal are. Normally appraisers use the standards drawn up by the Valuation Standards Committee of the Accounting Research and Development Foundation, but these standards and norms haven’t had any legal standing and there hasn’t been a national directive on standards. Norms and standards haven’t been applied or trusted in the courtroom context as a result. This has been a troubling phenomenon for appraisal personnel."

In addition to this, in the arts and creative sector there are a lot of artworks, patents, technologies and copyrighted works that need to be evaluated, but it's hard to secure a credible valuation report for them.

Before and After the Amendments

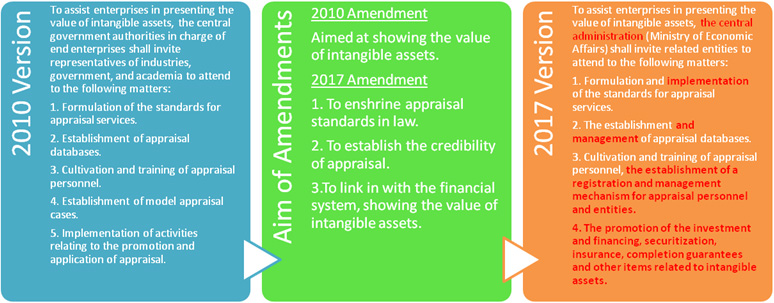

Figure 1 shows the differences pre and post amendment (See Figure 1).

Source: Chen’s presentation; Translated by Conor Stuart

On the left of Figure 1 is the 2010 version "To assist enterprises in presenting the value of intangible assets, the central government authorities in charge of end enterprises shall invite representatives of industries, government, and academia to attend to the following matters". Here Chen pointed out that in the Chinese language version of the statute, the language refers to "each central government authority" which suggests that there is no single supervisory authority but several of them, and therefore there is no specific person charged with taking responsibility for the valuation of intangible assets in Taiwan. In the 2017 version, the "central administration" refers directly to the Ministry of Economic Affairs, as this law was formulated by the Ministry of Economic Affairs, which means that it will be the ministry that is responsible for coordinating the different units for valuation work. This means that intangible asset evaluation finally has a unified supervisory authority, the Ministry of Economic Affairs.

Chen stated, when the Ministry of Economic Affairs was amending the law, they discovered that if they wanted credibility in the evaluation, they would have to establish unified evaluation standards and norms in a similar fashion to other countries. He pointed out that the Financial Regulatory Commission (FSC) and the Accounting Research and Development Foundation have already published twelve Statements of Valuation Standards, so it is hoped that these standards can be given legal standing and become national standards and norms.

In regards to the establishment of a valuation database, government databases already have data on the results of several research and development projects and the resulting transactions and they've previously published reports. Chen stated that in the future each government department can collate reports, which can then be used by domestic evaluators for reference purposes.

There are also complementary measures for financial organizations, as one of the biggest incentives for a company getting its intangible assets evaluated is to secure financing, so the Ministry of Economic Affairs will attempt to approach the issue by increasing credibility and establishing links to the financial system.

|

|

| Author: |

Conor Stuart |

| Current Post: |

Senior Editor, IP Observer |

| Education: |

MA Taiwanese Literature, National Taiwan University

BA Chinese and Spanish, Leeds University, UK |

| Experience: |

Translator/Editor, Want China Times

Editor, Erenlai Magazine |

|

|

|

| Facebook |

|

Follow the IP Observer on our FB Page |

|

|

|

|

|

|