The launch of the ASEAN Economic Community (AEC) on December 31, 2015, has led to a lot of hype concerning investment opportunities in what is now the seventh largest economic body in the world, but to what extent have trade barriers actually been lifted in the region?

The Association of Southeast Asian Nations (ASEAN) comprises Indonesia, Malaysia, the Philippines, Singapore, Thailand, Brunei, Cambodia, Laos, Myanmar and Vietnam. Its member states have a collective population of over 600 million and a collective GDP of US$2.5 trillion. It is also predicted to become the fifth largest economic body globally by 2020.

Chair professor of the Indian Council for Research on International Economic Relations’ (ICRIER) Trade Policy and the WTO Research Program Anwarul Hoda and Professor Rajeev Anantaram, who also works for ICRIER, benchmarked the progress of the various ASEAN members in facilitating trade at a recent seminar in Taipei.

Professor Anantaram stated of the AEC, “Bringing together a conglomeration of countries, so diverse, economically and politically, is a challenge,” going on to add, “The political economy of the region is such that, political practice always supersedes economic factors, and so, the old adage of ‘good economics is good politics’ only has limited kind of an impact in the ASEAN context.” He also pointed to the political diversity of ASEAN, which includes democracies and authoritative regimes and the economic disparity between its various members.

ASEAN was originally founded in 1967, with five founding members, Thailand, Singapore, Malaysia, Indonesia and the Philippines, later expanding to encompass all ten member countries. The AEC extends existing framework agreements, such as the 1992 Common Effective Preferential Tariff scheme, the ASEAN Framework Agreement on Services and the ASEAN Investment Area (AIA) initiative, which pitched the region as a potential global production base. Given the disparate speed of trade facilitation, the ten ASEAN countries are often divided into the ASEAN 6, comprising Indonesia, Thailand, Malaysia, the Philippines, Singapore and Brunei, seen as the most progressive economies in the association and the newer “CLMV” member countries – Cambodia, Laos, Myanmar and Vietnam – where progress on implementing the aims of the AEC is slower.

Professors Hoda and Anantaram used four key markers to benchmark progress:

Trade in goods

Trade in services

Trade facilitation

Investment

In terms of trade in goods, custom tariffs in the ASEAN 6 have been eliminated on 99.2% of goods, whereas in CLMV countries tariffs on 72.57% of goods have been eliminated. This means, as a whole, ASEAN member states have eliminated tariffs on 88.96% of goods. However, to qualify for tariff-free treatment, at least 40% of the components of any product must originate in the region.

Despite noting this progress on tariff barriers, Professor Anantaram stated that there was still a long way to go in terms of both non-tariff measures (NTMs) and tariff barriers. Mutual Recognition Agreements (MRAs) on standards, ensuring that products do not have to go through multiple tests, established in an agreement in 1998, have, as yet, only been applied to electronic and electrical goods and telecommunications equipment, but are still to be developed for agro-based products, automobiles and auto components where there has been slower progress, he said. There is also some work still to be done in terms of export controls, both in terms of taxation and quantitative restrictions. He gave the example of Indonesia’s imposition of a ban on the export of unprocessed minerals, as an example.

The 2003 ASEAN Harmonized Tariff Nomenclature (AHTN), which established a common customs classification system for goods has been fully implemented and a follow up agreement signed in 2005, aimed at establishing an ASEAN Single Window – preventing importers from having to approach different agencies in the same country for the same purpose – has been implemented by the ASEAN 6, but is still being put in place in CLMV countries.

According to data from the World Economic Forum, import and export tariffs are down across the board and there has been a dramatic decrease in red tape. This has also reduced the cost of logistics within the region, in which Singapore ranks top, not just regionally, but also globally, according to the World Bank Logistics Performance Index. The same index shows CLMV countries continuing to perform poorly in all six components of the index, however.

Supply of trade in services is classified into four modes, according to WTO’s General Agreement on Trade in Services (GATS):

Mode 1: Cross-border supply – “Service delivered within the territory of the Member, from the territory of another Member”

Mode 2: Consumption abroad – “Service delivered outside the territory of the Member, in the territory of another Member, to a service consumer of the Member”

Mode 3: Commercial Presence – “Service delivered within the territory of the Member, through the commercial presence of the supplier”

Mode 4: Presence of natural persons – “Service delivered within the territory of the Member, with supplier present as a natural person”

Anantaram stated that restrictions in four priority sections were set to be removed by 2010, namely air transport, e-ASEAN (ICT and e-commerce), healthcare and tourism, with logistics following in 2013, and all other sectors by 2015. Goods are now moving between different ASEAN countries several different time, due to the improvement in logistics.

No restrictions could be imposed on Mode 1 and Mode 2 without ‘bona fide’ regulatory purposes, with a more gradual liberalization of Mode 3, allowing 70% foreign equity by 2015, and the removal of market access and national treatment restrictions.

Progress on Mode 4 has been mixed, with Singapore forging ahead and CLMV countries trailing behind. Anantaram also stated that despite mutual recognition agreements (MRAs) on architectural services, accountancy services, surveying qualifications and medical practitioners in 2008, dental practitioners in 2009 and all other services in 2015, nationality or residence requirements for employment are proving an obstacle to liberalization in this mode and the liberalization applies only to professionals, not to semi-skilled or unskilled workers.

He added, however, that some member states maintain caps of below 70% on foreign equity in various service sectors, including hotels, telecom and healthcare.

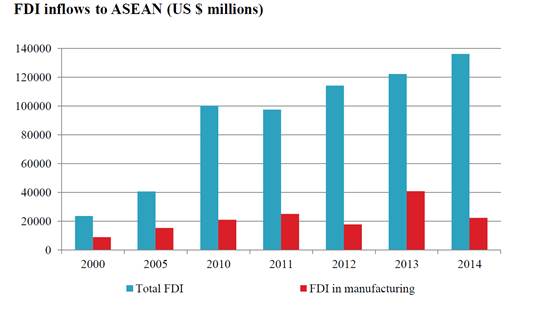

Professor Hoda then analyzed the economic effects of these steps towards trade liberalization, focusing on manufacturing. The FDI of the region has jumped dramatically over the last ten years from US$23.5 billion in 2000 to US$136 billion in 2014, which Hoda attributed to growing investor confidence fuelled by the stability in macroeconomic policy, the large market and the developed physical and human capital.

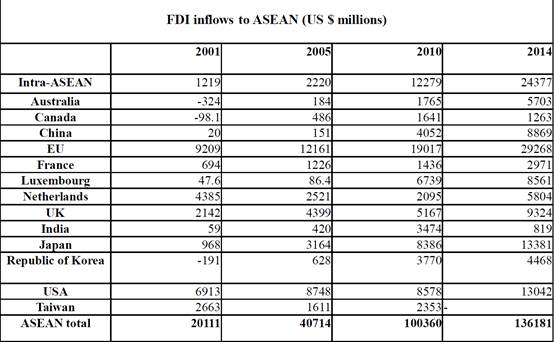

He stated that intra-ASEAN FDI played a big part in this, as Intra ASEAN FDI inflows jumped from US$800 million to US$22.8 billion over this period, with Singapore contributing 53% of the regional FDI. FDI inflows from outside ASEAN also rose steeply from US$22.8 billion to US$111.8 billion in the same period. The spread between external and intra-regional FDI inflows has insulated the region somewhat from shifts in global capital flows in the context of falling domestic investment, Hoda stated. He stated that ASEAN was now benefitting from FDI which would previously have been destined for China, which absorbed over 50% of FDI in the last 15-25 years. He suggested that investment in infrastructure would be key in spurring vertical FDI in the region. He also stated that as the Asian Financial Crisis continues to subside, regional investors have more credit in hand.

Many of the investors in the region from East Asia have seen these countries only as “a base for largely routine, low- end manufacturing, instead of places where R&D can be located and patents gained”, according to Anantaram, which is certainly true of the way ASEAN is viewed in Taiwan and China.

Hoda stated that the two groups of products that had been most successful in terms of the breakdown of trade barriers has been electric and electronic products, automotive components and hard disc drives.

Taiwanese investment in the ASEAN region peaked at US$5.8 billion in 2012, ASEAN exports to Taiwan rose from US$16.5 billion in 2000 to US$24 billion in 2013 and imports from Taiwan grew from US$18.9 billion to US$54.3 billion. ASEAN 6 exports of electrical and electronic products US$13.7 billion and imports of US$33.4 billion. Hoda attributed this to investment by Taiwanese entrepreneurs.

Lessons Learned:

To stimulate regional and global value chains barrier to international trade must be lowered along with logistics costs.

Investment by multinationals the starting point for regional and global value chains.

Industrial clusters develop around enterprises set up by multinational investors, which also lead to supply chain activity.

ASEAN has signed free trade agreements with six countries, China, India, Japan, South Korea, Australia and New Zealand and there are now plans to expand these agreements into the Regional Comprehensive Economic Partnership (RCEP), comprising the ASEAN + 6 countries, which should lead to further trade liberalization. Negotiations on the RCEP are set to resume in April.